News / 4 August 2025

Week in Review: Global stocks fall amid Tariff Concerns

The July employment report missed expectations by a wide margin. Nonfarm payrolls rose by just 73,000, well below the 100,000 forecast. More troubling were sharp downward revisions to previous months: June jobs were revised down to 14,000 (from 147,000) and May jobs fell to 19,000 (from 125,000). The unemployment rate ticked up to 4.2%, and the unexpectedly weak figures pushed Treasury yields lower as markets ramped up bets on a September Fed rate cut—now seen as more than 80% likely.

Meanwhile, U.S. economic growth moderated in the first half of the year amid subdued consumer activity and heightened trade policy uncertainty. Inflation-adjusted GDP expanded at an annualized rate of 3% in Q2, according to official data. However, average growth for the first half stood at just 1.25%, significantly below the 2024 pace, highlighting the broader slowdown in economic momentum

Among countries facing the steepest “reciprocal” tariffs, Syria has the highest rate at 41%. Exports from Laos and Myanmar to the U.S. will face a 40% duty. Switzerland and South Africa will be hit with tariffs of 39% and 30%, respectively. For some Asian nations that have not confirmed a trade pact with the U.S., the latest executive order offered some relief with lower duties. The new tariff rates on imports from Thailand will be lowered to

In local currency terms, the pan-European STOXX Europe 50 Index declined 3.5%, reflecting disappointment over the U.S.–EU trade framework. The UK’s FTSE 100 Index slipped 0.57%, supported in part by the weakening of the pound against the U.S. dollar. Robust eurozone economic data appeared to ease pressure on the European Central Bank to cut rates further. Headline inflation remained at 2.0% in July, slightly above the 1.9% forecast and matching the ECB’s target. GDP grew 0.1% in the second quarter, while the unemployment rate held steady at a record low of 6.2% in June.

Looking ahead, markets will remain focused on U.S. trade policy following the August 1 tariff announcement. Key U.S. data releases include the ISM Services PMI, trade balance, factory orders, and preliminary Q2 productivity and labor cost figures. Globally, monetary policy decisions are expected from the Bank of England, Reserve Bank of India, and Mexico’s central bank.

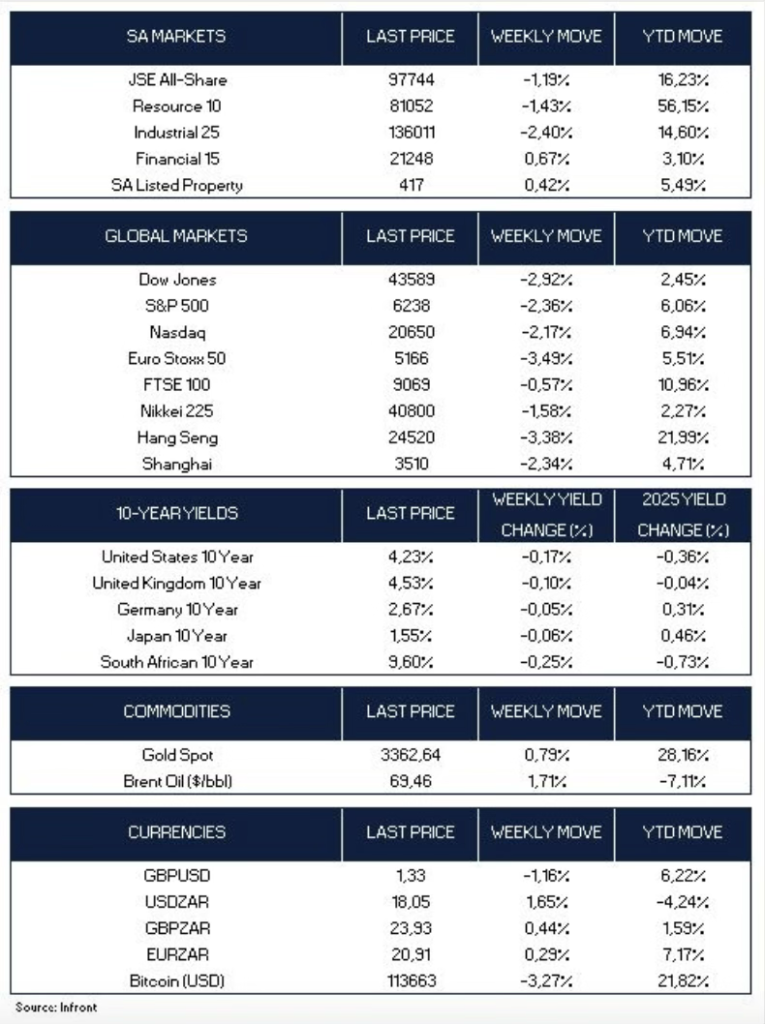

Market Moves of the Week

In a significant policy shift, the SARB effectively lowered its inflation target from 4.5% to 3%, moving focus from the midpoint to the lower bound of the 3–6% target range. National Treasury plans to address this change in its October Medium Term Budget Policy Statement.

Chart of the Week:

U.S. President Donald Trump signed an executive order on Thursday imposing “reciprocal” tariffs ranging from 10% to 41% on imports from dozens of countries and foreign locations, shortly after extending the deadline for a tariff deal with Mexico by another 90 days. The order listed higher import duty rates that would start from 7 August for 69 trading partners. Credits: Strategiq