News / 7 June 2026

Weekly Review: Stronger Data Shifts the Rate Debate

Global markets were reminded this week that good economic news is not always good news for investors. A stronger than expected U.S. jobs report showed that the labour market remains resilient, with hiring broadening across several sectors. While positive for growth, it also shifted the interest rate conversation. At the start of the year, markets were still expecting Fed rate cuts, but investors are now pricing in a much higher chance of further hikes.

Following the payrolls report, futures markets moved to a 68.4% probability of a Fed rate hike by December, although markets still expect the Fed to hold rates steady at its June meeting. The key concern is that a strong jobs market, sticky inflation and higher energy prices linked to Middle East tensions could force the Fed to keep rates higher for longer, or even tighten policy further.

In the U.S., equities started the week supported by continued optimism around artificial intelligence, but that momentum faded as investors reassessed a wider range of risks. The economy added 172,000 jobs in May, well ahead of expectations, while unemployment held steady at 4.3%. Job openings rose to 7.62 million, suggesting labour demand remains firm, although jobless claims moved higher and announced layoffs increased for a third consecutive month, with AI again cited as a leading reason for job cuts in parts of the technology sector.

Broader U.S. activity data also pointed to resilience, but with inflation still a concern. Manufacturing and services PMI readings improved, new orders strengthened and price pressures remained elevated. Together with higher oil prices, this weighed on bond markets, with the U.S. 10-year Treasury yield rising from 4.44% to around 4.55% as investors adjusted to a more uncertain interest rate outlook.

EUROPE & UK

In Europe, economic data pointed to a weaker growth backdrop. The eurozone economy contracted by 0.2% in the first quarter, a downgrade from the initial estimate of slight growth. Retail sales also disappointed, falling 0.4% in April, while services activity remained subdued. In the UK, manufacturing improved slightly, but services and construction weakened, and house prices fell more than expected. A brighter spot came from new car sales, which rose 7.1% year on year, supported by strong growth in electric and plug-in hybrid vehicles.

ASIA

Japan presented a mixed picture. Services activity slowed, with the Jibun Bank services PMI falling to 50.0 in May from 51.0, while wage growth remained encouraging. Nominal wages rose 3.5% year-on-year and real wages increased for a fourth consecutive month. However, household spending remained weak. The Bank of Japan also stayed in focus after Governor Kazuo Ueda signalled greater concern about inflation, raising the possibility of a June rate hike, while the yen weakened to around JPY 160 against the U.S. dollar.

China’s data was uneven, but not weak enough to suggest a major slowdown. The official manufacturing PMI eased to 50.0, showing that factory activity had lost momentum, while the private sector RatingDog manufacturing PMI remained in expansion territory at 51.8. Services were stronger, with the RatingDog services PMI improving to 54.4. AI also remained a key market theme in China, with Tencent reportedly testing an embedded AI agent for WeChat and DeepSeek attracting attention around a possible fundraising round.

GLOBAL EQUITIES

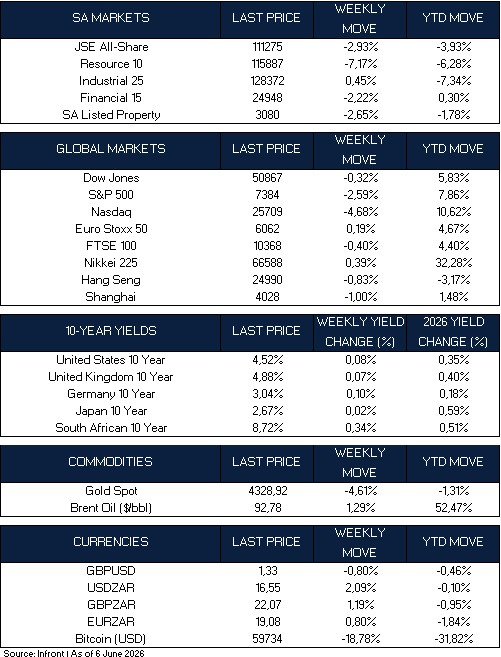

Overall, global markets ended the week on a cautious note. U.S. equities were under pressure, with the Dow Jones down 0.32%, the S&P 500 falling 2.59% and the Nasdaq declining 4.68%, although all three remain positive year to date. European and Asian markets were mixed, while bond yields rose across most major developed markets as investors adjusted to the possibility of higher interest rates for longer. In commodities, gold fell 4.61%, while Brent crude oil gained 1.29% and remains sharply higher year to date. Bitcoin was the weakest major risk asset, falling 18.78% for the week.

Market Moves of the Week:

South African economic data softened over the week, pointing to a loss of momentum after a stronger start to the quarter. The ABSA manufacturing PMI declined from 52.6 to 50.8 in May, while the S&P Global PMI slipped back into contractionary territory at 49.6. Business sentiment also weakened, with the RMB/BER Business Confidence Index falling to 39 in the second quarter from 47 previously.

Energy developments remained in focus after Eskom signed a long-term liquefied natural gas agreement with the Zululand Energy Terminal in Richards Bay. The agreement is intended to support Eskom’s planned 3,000MW gas-to-power project and forms part of South Africa’s broader shift toward gas as a transitional fuel. While the project still faces regulatory and legal hurdles, improved energy security remains an important longer-term driver for confidence and investment.

There were also notable corporate developments. Canal+ listed on the JSE following its acquisition of MultiChoice, while Amazon launched its Prime service in South Africa, highlighting the continued growth of online retail and competition in the local e-commerce market.

Against this backdrop, South African markets ended the week weaker. The JSE All Share Index declined 2.93%, with the sharpest pressure coming from resource shares, which fell 7.17% for the week and are now down 6.28% year to date. Financials declined 2.22%, while listed property softened by 2.65%. Industrials were the relative bright spot, gaining 0.45% for the week, although the sector remains under pressure year to date. The rand softened against major currencies, with the USD/ZAR at R16.55, while the South African 10-year government bond yield rose to 8.72%.

Chart of the Week:

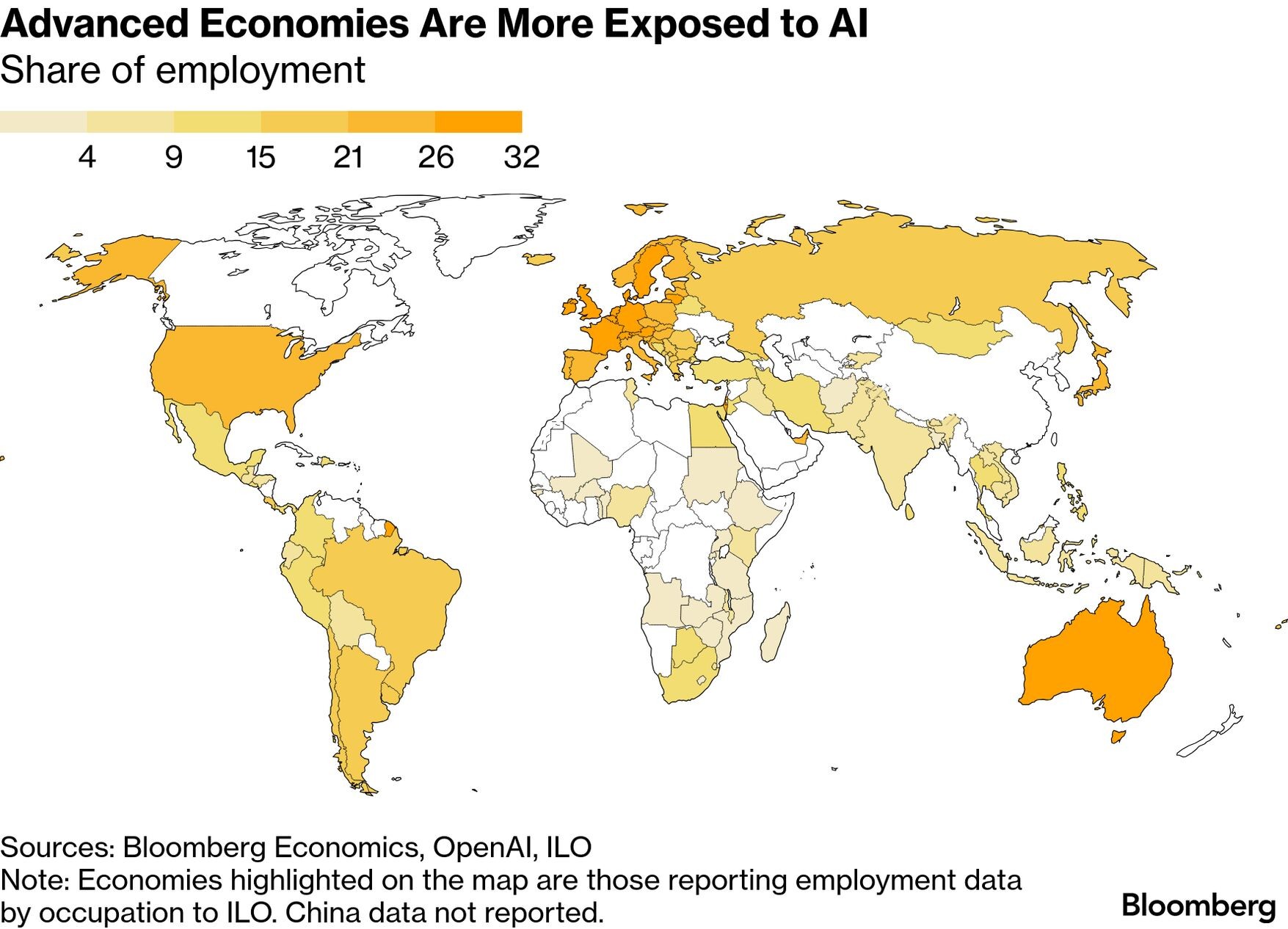

Fear of a “jobpocalypse” driven by artificial intelligence has become widespread since the launch of ChatGPT marked the unofficial beginning of the generative AI era. The chart shows that this risk is not evenly spread, with workers in advanced economies far more exposed to AI-related disruption than those in emerging markets. Bloomberg Economics estimates that around 27% of workers in advanced economies, or more than 120 million people across more than 30 countries, are likely to be meaningfully affected by AI. Yet despite the anxiety, and rising reports of AI-linked layoffs, the official labour market data has not yet shown evidence of a broad employment meltdown. Source: Bloomberg

Credits: Strategiq Capital