5 April 2026

Week in Review: Iran Conflict Stokes Inflation Fears

Global equity markets ended a volatile, holiday-shortened week in positive territory, with tentative signs of Middle East de-escalation lifting sentiment. The Nasdaq led the way, logging its best week since November, while the S&P 500 and Dow gained 3.36% and 2.96% respectively. European markets followed suit, with the STOXX 50 up 3.4% and the UK's FTSE 100 gaining 4.7%.

The mood swung sharply through the week. Equities rallied early on hopes the US campaign in Iran was nearing its end, only to reverse after Trump's Wednesday evening address threatened further escalation, including strikes on Iranian oil facilities over the next two to three weeks, while offering no plan to reopen the Strait of Hormuz. Markets largely recovered by Thursday's close.

Brent crude surged above $109/barrel, its highest level in nearly four years on renewed supply disruption fears, while gold rebounded nearly 4% to around $4,672/oz as the dollar strengthened and rate cut hopes faded. US Treasuries advanced, with the 10-year yield falling from 4.44% to 4.31%, aided by Fed Chair Powell's comments tempering near-term inflation concerns.

|

Eurozone inflation jumped to 2.5% in March from 1.9% in February, above the ECB's 2% target, driven by a 4.9% surge in energy costs. ECB President Lagarde signalled the central bank is monitoring the situation closely and stands ready to hike rates if necessary, even if the inflation spike proves temporary.

Japan's Nikkei fell 1.7% amid expectations the Bank of Japan may raise rates at its April meeting in response to oil-driven inflation pressures. Chinese markets were mixed, while Beijing and Islamabad jointly proposed a five-point peace plan calling for a ceasefire and protection of Strait of Hormuz shipping lanes.

Next week, focus remains on the Iran conflict as it enters its sixth week, alongside US CPI, FOMC minutes, the PCE report, Michigan Consumer Sentiment, and monetary policy decisions from the Reserve Bank of India.

Market Moves of the Week

South African Revenue Service (SARS) collected a net R2.01 trillion in tax for the fiscal year ended 31 March, 8.4% higher year-on-year and R24.7 billion above the 2025 budget forecast. The agency credited compliance initiatives, improved efficiency, and a strong contribution from the mining sector. For 2026/27, SARS is targeting R2.13 trillion, a 5.8% increase.

President Ramaphosa has appointed Ngobani Makhubu as the new SARS Commissioner for five years, effective 1 May. Makhubu, currently Deputy Commissioner for Taxpayer Engagement and Operations, takes over from Edward Kieswetter, who steps down after seven years at the helm.

On the fuel front, petrol rose R3.06/litre to R23.25 from 1 April, while inland diesel hit a record R26.11/litre, up R7.51. The Iran conflict, which has pushed Brent above $100/barrel and pressured the rand, is the primary driver. A R3/litre fuel levy cut softened the blow, without it, economists warned the increase could have added at least 1.0 percentage point to annual CPI in April. February CPI came in at 3.0% year-on-year, bang on the SARB's target, leaving little room for an unmanaged fuel shock.

Markets recovered some recent losses, with the FTSE/JSE All Share ending the holiday-shortened week 3.9% higher, buoyed by resource counters. The rand also firmed, gaining over 1% to close at R16.92/$.dollar, while the South African 10-year government bond yield edged slightly lower to 9.19%.

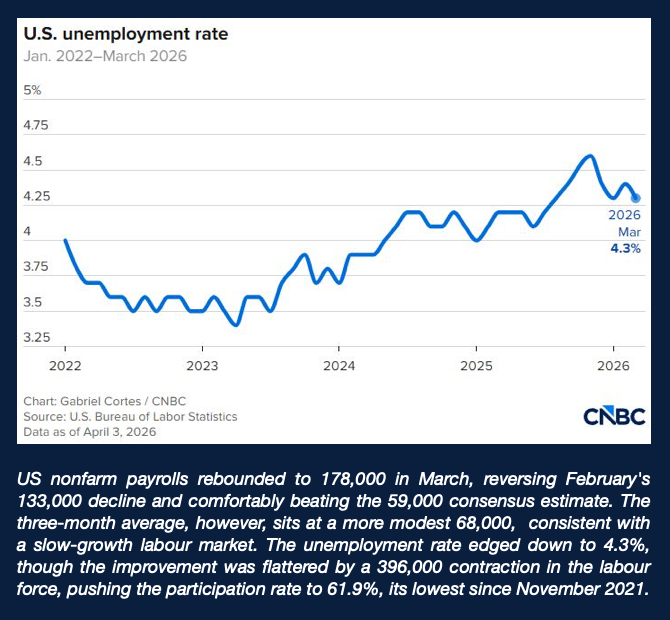

Chart of the Week:

.Credits: Strategiq

___________________________________________________________________

CAPTA Wealth offers our clients a wide range of options and solutions when it comes to investing in global markets. Contact us for more information about how we can ensure your portfolio is generating the maximum returns. Our offices around the country and offshore, are poised for wealth creation. Let us focus on yours.

YOUR WEALTH IS OUR FOCUS

© 2026 CAPTA Wealth