25 January 2026

Week in Review: Volatility Flares, Fundamentals Hold

Global markets navigated another week shaped by geopolitical uncertainty and shifting investor sentiment, as renewed U.S. tariff threats briefly unsettled risk appetite before attention returned to economic data and corporate earnings. A fresh round of company earnings is testing whether the AI-driven profit cycle is broadening beyond a narrow group of technology leaders, while recent geopolitical developments underscored how quickly policy uncertainty can re-emerge and influence market confidence. Although volatility proved short-lived, the episode highlighted the persistent tension between political risk and economic fundamentals that continues to define the global investment landscape.

In the United States, markets were initially rattled by an escalation in tariff rhetoric linked to President Trump’s push to acquire Greenland, triggering a sharp risk-off reaction. U.S. equities declined, the dollar weakened, Treasury yields fell and gold surged to record highs, briefly reviving the “sell America” narrative that had emerged at times in 2025. Sentiment improved later in the week after Trump softened his stance and signalled a potential framework for a deal, allowing markets to stabilise. Beneath the political headlines, economic data remained broadly resilient: real GDP growth was revised higher to an annualised 4.4% in the third quarter, core inflation held at 2.8% year-on-year, jobless claims remained near historically low levels and business activity indicators showed modest improvement. Together, these data suggest the U.S. economy continues to expand at a solid pace, even as political uncertainty injects episodic volatility.

|

|

Market Moves of the Week

The South African rand strengthened over the week, closing near R16.10/$ as markets positioned ahead of the upcoming interest rate decision and continued to price in supportive global and domestic dynamics. The currency remains close to its strongest levels since mid-2022, underpinned by record-high gold prices, improved fiscal metrics, a credible monetary policy framework and a softer U.S. dollar. The rand has gained more than 2% against the dollar since the start of 2026, with further upside possible should commodity prices remain firm and global risk sentiment stay supportive. However, structural constraints, including weak domestic growth prospects and the currency’s inherent volatility, suggest that recent gains remain vulnerable to shifts in global conditions.

On the macro front, inflation remains well contained, reinforcing expectations that monetary conditions could gradually ease in the year ahead. Consumer inflation rose 0.2% month-on-month in December, following a decline in the previous month, while headline CPI increased to 3.6% year-on-year from 3.5%, remaining within the Reserve Bank’s target range. Domestic data painted a mixed picture: retail sales rose 0.6% month-on-month in November and accelerated to 3.5% year-on-year, signalling resilient consumer activity, while mining production deteriorated, falling 5.9% month-on-month and declining 2.7% year-on-year, marking a sharp reversal from the prior month’s gains. Overall, South Africa’s macro environment reflects a cautiously improving inflation backdrop and resilient consumption, tempered by ongoing weakness in the mining sector and a still subdued growth outlook.

Local equities advanced over the week, with the JSE All Share Index rising 1.76%, supported by a strong rebound in resource stocks (+7.16%) and solid gains in financials (+1.18%), while listed property also advanced (+0.75%). Industrials lagged the broader market, declining 3.02%. The rand strengthened against the U.S. dollar to around 16.10, while the 10-year South African government bond yield declined to 8.15%, reflecting improved sentiment in local fixed income markets.

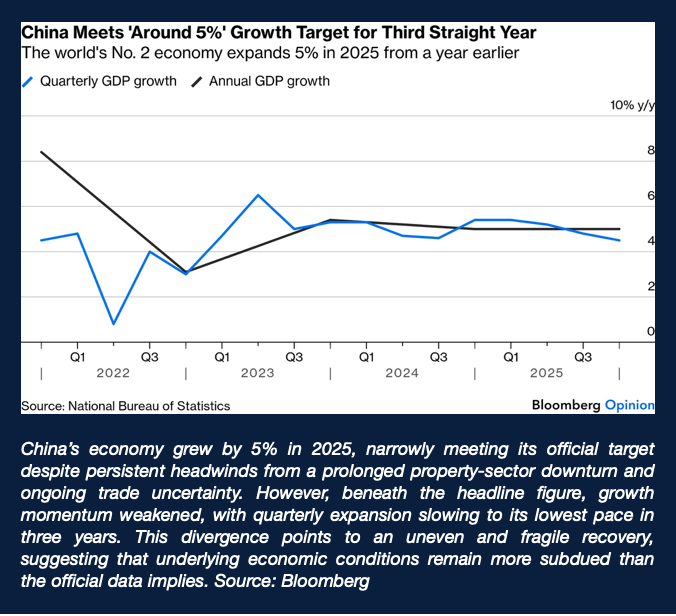

Chart of the Week:

.Credits: Strategiq

___________________________________________________________________

CAPTA Wealth offers our clients a wide range of options and solutions when it comes to investing in global markets. Contact us for more information about how we can ensure your portfolio is generating the maximum returns. Our offices around the country and offshore, are poised for wealth creation. Let us focus on yours.

YOUR WEALTH IS OUR FOCUS

© 2026 CAPTA Wealth