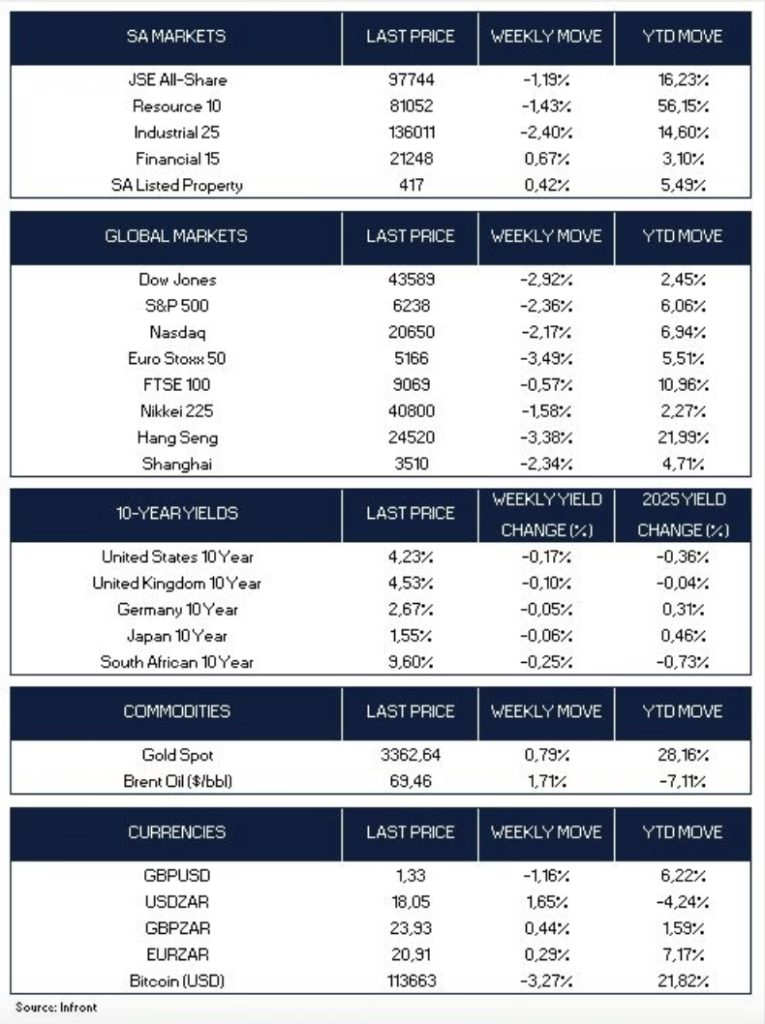

U.S. equities closed the week significantly lower, with major indices recording their steepest declines since the tariff-driven sell-off in early April. The downturn followed the expiration of President Trump’s 90-day moratorium on proposed “reciprocal” tariffs, compounded by the release of a weaker-than-expected July employment report. All three major indexes ended the week in negative territory: the S&P 500 fell 2.4%, marking its worst weekly performance since May 23; the Dow Jones Industrial Average declined 2.9%, its sharpest weekly loss since April 4; and the Nasdaq Composite retreated 2.2% over the same period.

The July employment report missed expectations by a wide margin. Nonfarm payrolls rose by just 73,000, well below the 100,000 forecast. More troubling were sharp downward revisions to previous months: June jobs were revised down to 14,000 (from 147,000) and May jobs fell to 19,000 (from 125,000). The unemployment rate ticked up to 4.2%, and the unexpectedly weak figures pushed Treasury yields lower as markets ramped up bets on a September Fed rate cut—now seen as more than 80% likely.

The Federal Reserve concluded its July monetary policy meeting on Wednesday, opting—as widely anticipated—to maintain the target federal funds rate within the range of 4.25% to 4.50%. However, the decision was not unanimous, with Governors Michelle Bowman and Christopher Waller dissenting in favour of a 25 basis point cut. The FOMC’s statement noted that economic activity had moderated in the first half of the year, a detail viewed by some investors as dovish.

In his post-meeting press conference, Chair Jerome Powell reaffirmed the Fed’s data-dependent approach, emphasizing that inflation remains above target and that no decisions had been made regarding a potential rate cut in September. His comments, combined with concerns over the inflationary impact of new tariffs, tempered market expectations for near-term easing.

Data released by the Bureau of Economic Analysis (BEA) on Thursday revealed that inflation picked up in June, adding complexity to the Federal Reserve’s policy outlook. The core Personal Consumption Expenditures (PCE) index—the Fed’s preferred inflation gauge—rose 0.3% month over month, up from 0.2% in May. On an annual basis, core PCE increased 2.8%, remaining well above the Fed’s 2% target and marking one of the fastest monthly gains this year.

At the same time, consumer spending showed minimal growth, reflecting underlying economic softness. Real disposable income was flat, following a decline in May, while wages and salaries posted only modest gains, suggesting a cooling labour market.

Meanwhile, U.S. economic growth moderated in the first half of the year amid subdued consumer activity and heightened trade policy uncertainty. Inflation-adjusted GDP expanded at an annualized rate of 3% in Q2, according to official data. However, average growth for the first half stood at just 1.25%, significantly below the 2024 pace, highlighting the broader slowdown in economic momentum

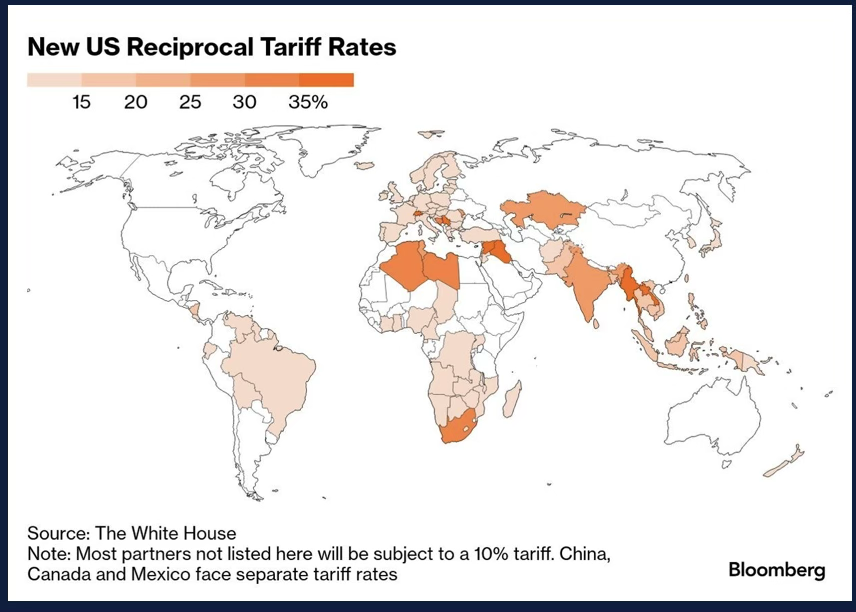

On Thursday, President Trump signed an executive order imposing increased tariffs on the majority of U.S. trading partners, with updated duties ranging from 10% to 41% effective August 7. The announcement followed a series of developments throughout the week, including new trade agreements with the European Union and South Korea, as well as a 90-day extension for ongoing negotiations with Mexico.

Among countries facing the steepest “reciprocal” tariffs, Syria has the highest rate at 41%. Exports from Laos and Myanmar to the U.S. will face a 40% duty. Switzerland and South Africa will be hit with tariffs of 39% and 30%, respectively. For some Asian nations that have not confirmed a trade pact with the U.S., the latest executive order offered some relief with lower duties. The new tariff rates on imports from Thailand will be lowered to

In local currency terms, the pan-European STOXX Europe 50 Index declined 3.5%, reflecting disappointment over the U.S.–EU trade framework. The UK’s FTSE 100 Index slipped 0.57%, supported in part by the weakening of the pound against the U.S. dollar. Robust eurozone economic data appeared to ease pressure on the European Central Bank to cut rates further. Headline inflation remained at 2.0% in July, slightly above the 1.9% forecast and matching the ECB’s target. GDP grew 0.1% in the second quarter, while the unemployment rate held steady at a record low of 6.2% in June.

In Japan, equity markets declined, with the Nikkei 225 down 1.58% while the 10-year government bond yield slipped to 1.55%. As expected, the Bank of Japan kept its policy rate unchanged at 0.5% and raised its core CPI forecast for FY2025 to 2.7%, citing continued food price inflation.

Chinese markets retreated amid concerns over new U.S. tariffs and signs of domestic economic slowing with recent PMI data pointed to sluggish domestic demand and persistent global uncertainty. The benchmark Shanghai Composite lost 2.3%, while Hong Kong’s Hang Seng Index dropped 3.4%.

Commodity markets were mixed. Spot gold rose nearly 2% to above $3,350 per ounce on expectations of a U.S. rate cut, following signs of labour market cooling, while Brent crude futures fell 2.8% to $69.70 per barrel on speculation that OPEC+ may agree to increase output by 548,000 barrels per day in September.

Looking ahead, markets will remain focused on U.S. trade policy following the August 1 tariff announcement. Key U.S. data releases include the ISM Services PMI, trade balance, factory orders, and preliminary Q2 productivity and labor cost figures. Globally, monetary policy decisions are expected from the Bank of England, Reserve Bank of India, and Mexico’s central bank.

Market Moves of the Week

The JSE experienced its largest intraday decline since June 13 on Friday, reacting to the imminent expiration of a key deadline to avoid new U.S. tariffs on South African exports. The long-anticipated 30% tariff, set to take effect in seven days, triggered a broad sell-off after South Africa’s efforts to negotiate a more favourable trade agreement with the Trump administration failed. In response, the Department of Trade, Industry and Competition (DTIC) announced mitigating measures to ease the impact.

The All Share ended the week 1.19% lower, led by declines in industrial and resource stocks. The rand weakened to R18.29 against the dollar in early trade on Friday – its lowest level since 7 May, before recouping some losses to end the week at R18.05/$.

On Thursday, the South African Reserve Bank’s (SARB) Monetary Policy Committee cut the repo rate, citing improved domestic economic conditions. The July MPC meeting, which unanimously approved the 25bp cut, also revised inflation forecasts downward by 0.9 and 1.4 percentage points for 2026 and 2027, respectively, to 3.3% and 3.0%. The bank adjusted its GDP growth forecast, lowering 2026 expectations by 0.2 percentage points to 1.3%, while raising the 2027 outlook by 0.2 percentage points to 2.0%, citing balanced risks to growth and inflation.

In a significant policy shift, the SARB effectively lowered its inflation target from 4.5% to 3%, moving focus from the midpoint to the lower bound of the 3–6% target range. National Treasury plans to address this change in its October Medium Term Budget Policy Statement.

Chart of the Week:

U.S. President Donald Trump signed an executive order on Thursday imposing “reciprocal” tariffs ranging from 10% to 41% on imports from dozens of countries and foreign locations, shortly after extending the deadline for a tariff deal with Mexico by another 90 days. The order listed higher import duty rates that would start from 7 August for 69 trading partners.

Credits: Strategiq

© 2026 CAPTA Wealth