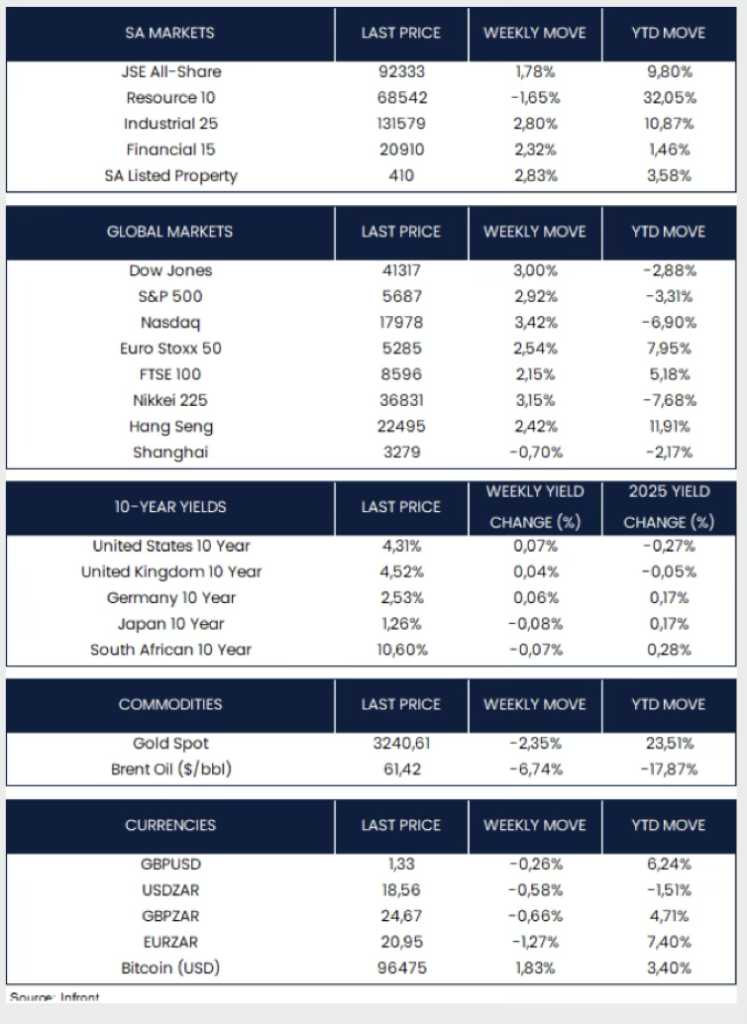

Eurozone economic growth picked up to 0.4% in Q1, doubling the prior quarter’s pace and beating the 0.2% consensus forecast from FactSet. In other news, Bloomberg reported that the European Union plans to ease trade barriers with the U.S., boost investment, cooperate on strategic issues, and increase purchases of U.S. goods like LNG and tech. The Euro Stoxx 50 index ended the week up 2.5% while the FTSE 100 gained 2.2%.

U.S. stocks ended the week higher, with the S&P 500 (+2.9%) posting a second straight weekly gain and a nine-day winning streak. The index erased the early April 13.8% drop amid solid earnings reports, hopes for a lessening of the US–China trade friction, and resilient U.S. labour data. The Nasdaq jumped 3.4% on strong tech earnings, while small and mid-caps rose for a fourth consecutive week. The Dow Jones gained 3% on the week.

Late in the week, attention turned to earnings, with companies representing nearly 40% of the S&P 500’s market cap - including four Magnificent Seven names - reporting Q1 results. Despite limited forward guidance due to trade uncertainty, sentiment stayed upbeat as investors bet on resilience amid slowing growth and tariff risks.

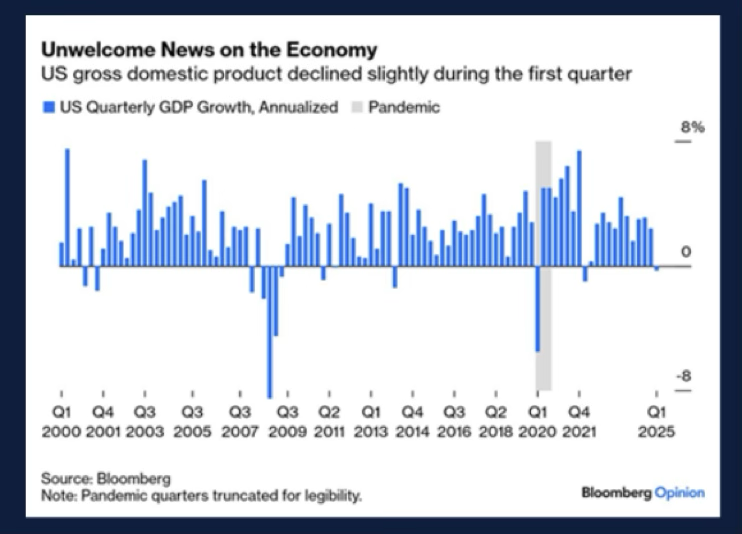

The week’s U.S. economic data offered mixed signals. Job openings fell to a seven-month low, and ADP reported a sharp slowdown in private payroll growth. However, Friday’s official jobs report beat expectations with 177,000 new jobs, steady unemployment at 4.2%, and modest wage growth, lifting market sentiment. The BEA’s advance estimate showed the U.S. economy contracted 0.3% in Q1 - the first decline since 2022 - driven by weaker consumer and government spending and a surge in imports, likely tied to businesses front-loading ahead of new tariffs.

Japanese stocks advanced for the week, with the Nikkei 225 up 3.2%. The Bank of Japan kept interest rates unchanged Thursday but lowered its growth forecast for the fiscal year ending March 2026 to 0.5%, down from 1.1%, citing export pressures from U.S. tariffs.

China will remove tariffs on certain U.S. imports, such as semiconductors, chipmaking equipment, medical supplies, and aviation parts, that cannot be sourced elsewhere. Beijing also introduced measures to support exporters and stimulate domestic consumption to offset U.S. tariffs. The tech-heavy Hang Seng index ended the week up 3.2%, while the broader Shanghai index dipped 0.7%.

On the commodity front, “safe haven” Gold fell 2.4% over the week, while Brent oil slumped 6.7% after Saudi Arabia signalled it might increase oil production.

Market Moves of the Week

South Africa’s seasonally adjusted Absa Purchasing Managers’ Index (PMI) fell to 44.7 in April 2025 from 48.7 in March, marking the sixth straight month of contraction in manufacturing activity and signalling a sharp overall decline. Survey participants pointed to global trade tensions, political uncertainty at home, heavy rainfall, and the return of scheduled power outages as key factors behind the weak sentiment.

During a media briefing on Wednesday, Finance Minister Enoch Godongwana announced that the third Budget speech is scheduled for 21 May. This follows last week's reversal of the proposed 0.5% VAT increase, originally included in the March 2025 Budget. The Minister also stated that neither he nor the Treasury will be responding to questions about the budget's preparation ahead of the 21 May address.

The All-Share Index rose 1.8% for the week, in line with global markets, despite a 1.7% decline in Resources. The local currency strengthened against the U.S. dollar, moving from R18.67/$ to R18.56/$ w/w. South Africa’s 10-year government bond yield fell by 7 bps.

Chart of the Week:

Wednesday brought the news that the first estimate of gross domestic product for the quarter ended March 2025 declined 0.3%, only the second quarterly fall since the pandemic and the first in three years. Source: Bloomberg.

Credits: Strategic IQ

© 2026 CAPTA Wealth