8 February 2026

Week in Review: Markets Rotate as Technology Leadership Pauses

Global markets delivered a mixed performance this week as investors navigated a combination of economic data, shifting policy expectations and evolving sector leadership. While overall index movements were relatively contained, underlying market dynamics pointed to a continued rotation away from narrow technology leadership toward more cyclical and value-oriented areas.

In the United States, equity markets ended the week divided. The Nasdaq declined 1.84%, reflecting pressure on large-cap technology shares, while the S&P 500 was broadly unchanged at -0.10%. In contrast, the Dow Jones Industrial Average rose 2.50%, supported by gains in more traditional and cyclical sectors. The week highlighted a shift in investor positioning, as concerns around the pace of artificial intelligence investment and its impact on corporate profitability weighed on high-growth companies that have driven market returns in recent years. At the same time, investors rotated into areas of the market that have lagged, including financials and industrials, which benefited from improving economic expectations.

Economic data releases added to the cautious tone. Labour market indicators were softer than anticipated, with slower private job creation, a decline in job openings to their lowest level since 2020 and a notable rise in layoffs. Despite this, parts of the real economy showed resilience. Manufacturing activity returned to expansion territory for the first time in a year, supported by stronger new orders, while services activity remained stable and continued to expand. In fixed income markets, U.S. Treasury yields edged lower, supporting bond returns, as investors positioned more defensively amid mixed economic signals.

|

Market Moves of the Week

South African markets were relatively stable, with the JSE All Share finishing the week unchanged. Performance across sectors was mixed, with financials and listed property posting gains while resources declined amid commodity volatility and industrials were largely flat. The domestic bond market was steady, with the 10-year government yield closing around 8.06%.

On the policy front, South Africa moved to deepen its economic relationship with China through the signing of a new framework agreement aimed at expanding trade and investment ties. The agreement is expected to improve access for South African exports into Chinese markets while encouraging further Chinese investment across sectors such as mining, agriculture, renewable energy and manufacturing. Although still in its early stages, the initiative signals growing economic cooperation and could support longer-term growth and employment prospects.

Overall, the week reinforced a key theme shaping global markets: leadership is broadening. After an extended period dominated by large-cap technology, investors are increasingly allocating toward value-oriented sectors, cyclical industries and regions outside the United States. Economic data remains mixed, with labour markets softening in some areas while manufacturing stabilises and inflation continues to ease. For long-term investors, this environment supports the case for diversification across geographies, asset classes and sectors, as markets adjust to shifting growth expectations and evolving monetary policy paths.

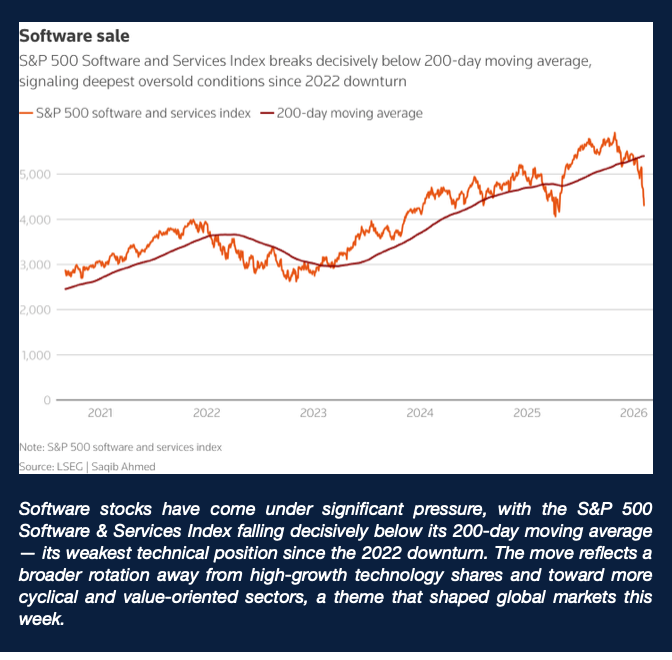

Chart of the Week:

.Credits: Strategiq

___________________________________________________________________

CAPTA Wealth offers our clients a wide range of options and solutions when it comes to investing in global markets. Contact us for more information about how we can ensure your portfolio is generating the maximum returns. Our offices around the country and offshore, are poised for wealth creation. Let us focus on yours.

YOUR WEALTH IS OUR FOCUS

© 2026 CAPTA Wealth