11 January 2026

Week in Review: US hiring slows and SA PMI disappoints, but markets hold firm

US markets began the year on a confident footing. The Dow Jones rose 2.32% over the week, while the S&P 500 gained 1.57% and the Nasdaq advanced 1.88%. This was not just a technology-driven rally. Smaller companies and value-oriented shares outperformed, which signals growing confidence in the broader economy.

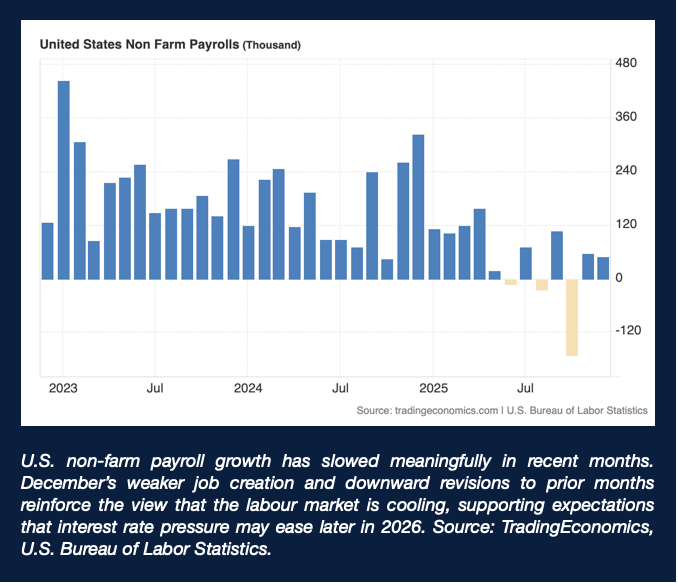

Beneath the market strength, the economic data was more nuanced. Job growth slowed sharply in December and prior months were revised lower, confirming that the labour market is cooling. Job openings also declined, which points to easing demand for workers. Manufacturing remains under pressure, with activity still contracting, but the services sector continues to show resilience and even signs of improvement.

European equities built on improving sentiment this week. The Euro Stoxx 50 rose 2.51% and the FTSE 100 gained 1.74%, reflecting growing optimism that the region may be stabilising after a difficult period. Economic data helped support this view. Industrial production and manufacturing orders in Germany surprised positively, while retail sales across the eurozone also exceeded expectations. Inflation eased to 2.0%, which is exactly in line with the European Central Bank’s target and a welcome development for consumers and businesses. That said, the outlook is not without risks. Services inflation remains elevated, which means interest rates are likely to stay higher for longer. In the UK, housing data showed ongoing softness, with mortgage approvals slipping and house prices falling again in December. This continues to weigh on household confidence. Overall, Europe is showing signs of progress, but the recovery remains uneven. Market returns this week reflect cautious optimism rather than full conviction. |

|

China delivered a split performance this week. The Shanghai Composite rose 3.82%, driven by enthusiasm around artificial intelligence and domestic technology stocks, while Hong Kong’s Hang Seng declined 0.39%, highlighting the uneven nature of investor sentiment. Trading activity in mainland markets has increased sharply and retail participation remains elevated, which reflects strong speculative interest in selected sectors. However, the economic backdrop remains fragile. Consumer inflation has improved modestly, but producer prices are still falling year on year, which continues to pressure corporate profitability. China remains heavily dependent on policy support. Investors are watching closely for further stimulus measures in 2026, as additional easing could meaningfully influence both economic growth and market performance. This remains a market with significant upside potential, but also elevated risk, which reinforces the importance of maintaining balanced exposure. Japan was one of the strongest performers globally this week. The Nikkei 225 rose 3.18%, supported by strong gains in technology shares and a weaker yen, which benefits export-oriented companies. Encouragingly, the economic backdrop is also improving. Household spending rebounded strongly in November, driven by higher spending on vehicles and everyday consumption such as food and dining. This suggests that Japanese consumers are becoming more confident again, even though real wages remain under pressure. The Bank of Japan continues to signal that interest rates may rise gradually during 2026 as inflation and growth become more sustainable. Markets appear comfortable with this path, viewing it as a sign of economic normalisation rather than a threat to growth. |

|

Market Moves of the Week

Local markets posted positive returns over the week. The JSE All Share gained 1.74%, with resources performing particularly well as the Resources 10 Index rose 3.86%. Financials gained 1.06%, industrial shares rose 0.49%, and listed property advanced 1.89%.

Despite the positive market performance, the economic data continues to paint a challenging picture. The Absa Purchasing Managers’ Index fell to 40.5 in December, the weakest reading since the lockdown period. This confirms that South Africa’s manufacturing sector remains in contraction and under significant strain.

The weakness was driven by falling employment and declining inventories, both of which signal soft demand conditions. While business activity showed some improvement, economists broadly agree that manufacturing is likely to drag on growth into 2026. GDP growth expectations remain subdued at around 1.0% to 1.3%.

There was, however, one encouraging signal. Business expectations for the next six months improved sharply, suggesting that confidence could recover if conditions stabilise and operational challenges ease.

For investors, this reinforces the importance of maintaining offshore diversification while selectively taking advantage of opportunities within the local market.

Chart of the Week:

.Credits: Strategiq

___________________________________________________________________

CAPTA Wealth offers our clients a wide range of options and solutions when it comes to investing in global markets. Contact us for more information about how we can ensure your portfolio is generating the maximum returns. Our offices around the country and offshore, are poised for wealth creation. Let us focus on yours.

YOUR WEALTH IS OUR FOCUS