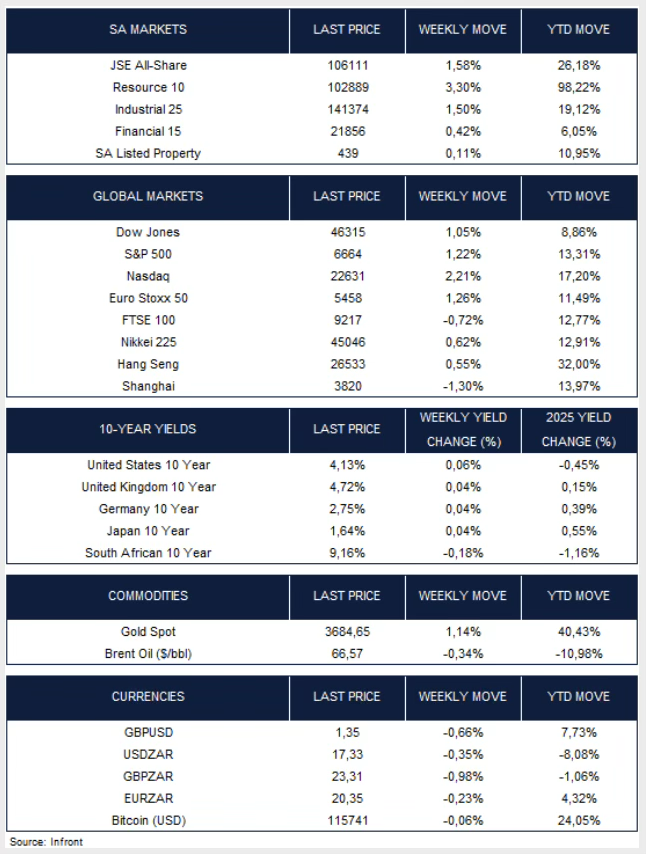

Major U.S. stock indexes hit record highs during the week. The Nasdaq Composite advanced 2.21%, while the S&P 500 and Dow Jones Industrial Average gained 1.22% and 1.05%, respectively. Meanwhile, the yield on the U.S. 10-year Treasury note rose 6 basis points to 4.13%.

The Federal Reserve lowered rates by 25 basis points on Wednesday, as widely expected, and indicated it may cut by a further 50 basis points before year-end. Policymakers flagged rising downside risks to employment, even as inflation remains elevated. Governor Stephen Miran, newly appointed to the Board, was the lone dissenter, preferring a larger 50-basis-point reduction. Chair Jerome Powell framed the move as a risk-management measure to pre-empt further labour market softening.

In other economic news, U.S. retail sales jumped 0.6% in August, surpassing expectations, while core sales climbed 0.7%, also beating forecasts. July figures were revised higher, showing 0.6% growth instead of the initially reported 0.5%. Despite signs of a softer labour market, economic activity appears to remain resilient.

President Trump and Chinese President Xi Jinping spoke by phone on Friday. Chinese state media described the talks as “pragmatic and constructive.” Xi emphasised the importance of US-China relations, urged Washington to avoid unilateral trade actions, and expressed support for a TikTok resolution that separates its U.S. operations from its Chinese parent. Trump said on social media that the TikTok deal was approved and progress was made on trade, fentanyl, and the Russia-Ukraine conflict. The leaders are set to meet at the APEC Summit in late October, with Trump planning a visit to China in early 2026.

The Bank of England this week held its key rate at 4% in a 7–2 vote and slowed bond sales to ease gilt market pressures amid rising long-term yields. Governor Andrew Bailey said that while inflation is expected to return to the 2% target, any future rate cuts will need to be gradual and cautious. Economic data showed headline inflation steady at 3.8% in August, overall wage growth rising to 4.7% and unemployment holding at 4.7%. On the market front, the FTSE 100 fell 0.72% week-on-week, while Europe’s Euro Stoxx 50 gained 1.26%.

Japan’s stock market edged higher this week, with the Nikkei 225 rising 0.62%. The Bank of Japan surprised markets by announcing it would start selling its ETF and REIT holdings sooner than expected, signalling a shift toward policy normalisation. As widely expected, interest rates were kept at 0.50%, though two policymakers broke from consensus, favouring a hike amid ongoing political and trade uncertainties.

Mainland Chinese stocks fell as investors booked profits amid signs of slowing growth. The Shanghai Composite fell 1.3%, while Hong Kong’s Hang Seng rose 0.55%. August data showed retail sales and industrial output posting their weakest monthly growth this year, with fixed asset investment slowing to just 0.5% for the first eight months, the lowest non-pandemic reading on record.

In commodities, Brent oil dipped 0.34% on the week, while gold advanced 1.14% as investors reacted to the Federal Reserve’s first rate cut of the year and monitored signals on future policy.

Market Moves of the Week

The South African Reserve Bank paused its rate-cutting cycle on Thursday, leaving the benchmark repo rate unchanged at 7%, following a split 4-2 vote, with two dissenting members in favour of a 25-basis point cut. This decision aligned with market expectations. The bank's updated forecasts were slightly more hawkish, revising the 2026 inflation projection from 3.3% to 3.6%, driven by supply-side factors such as food and fuel prices, as well as higher electricity tariffs. The Monetary Policy Committee (MPC) highlighted that it is closely monitoring the effects of the 125 basis points of rate cuts implemented over the past year, along with shifts in inflation expectations and associated risks, before considering any further easing.

South African (SA) inflation slowed more than expected in August, driven by lower fuel and food costs. Headline consumer inflation fell to 3.3% y/y from 3.5% in July, lower than the 3.6% forecast of economists polled by Reuters. The annual core inflation rate, which excludes food, non-alcoholic beverages, fuel, and energy, rose to 3.1% in August 2025, the highest since March, from 3% in the prior month.

SA’s manufacturing sector slipped back into contraction in August, with the Absa PMI falling 1.4 points to 49.5 after briefly entering expansion in July. Compiled by the Bureau for Economic Research (BER), the index highlights weak domestic and export demand, as new sales orders dropped sharply to 47.4, with respondents citing the adverse effects of U.S. tariffs on exports.

The All-Share Index rose 1.58% this week, boosted by Resources and Industrials. The local currency strengthened against the U.S. dollar, moving to R17.33/$ from last week’s R17.39/$ level. The 10-year SA government bond extended its year-to-date rally, with yields falling 18 basis points over the week.

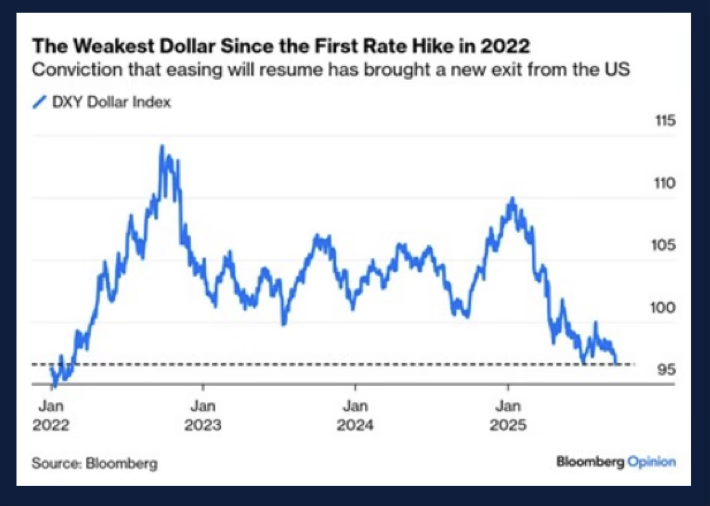

Chart of the Week:

The dollar dropped this week to its lowest level since the start of the Fed’s 2022 rate-hike cycle.This is what President Donald Trump’s administration wants and eases financial conditions for anyone around the world who needs to finance in dollars. Source: Bloomberg.

Credits: Strategiq

© 2026 CAPTA Wealth