Eurozone inflation edged up in June, with the headline rate reaching the ECB’s 2.0% target, up from 1.9% in May. Core inflation remained steady at 2.3%, signalling persistent underlying price pressures. Services inflation rose slightly to 3.3% from 3.2%, underscoring ongoing challenges in bringing inflation sustainably to target.

U.S. lawmakers made meaningful progress on the long-debated budget reconciliation bill this week. The Senate passed the legislation on Tuesday, and the House approved it Thursday afternoon after a lengthy speech by House Minority Leader Hakeem Jeffries briefly that delayed proceedings. With a key procedural hurdle cleared earlier that day, the bill now awaits final adoption.

Meanwhile, the U.S. Labor Department reported 147,000 jobs added in June—exceeding expectations and up from May’s revised 144,000. The unemployment rate edged down to 4.1%, and average hourly earnings rose 0.2% month over month. This stronger report followed a surprise 33,000 drop in private payrolls from ADP data earlier in the week—the first decline since March 2023.

U.S. manufacturing contracted for the fourth consecutive month in June. The ISM Manufacturing PMI rose slightly to 49.0 from 48.5 in May, indicating slower contraction but remaining below the 50.0 expansion mark. Softer demand and uncertainty weighed on factory activity. In contrast, the services sector showed resilience, with the ISM Services PMI climbing into expansion at 50.8, driven by stronger business activity and new orders.

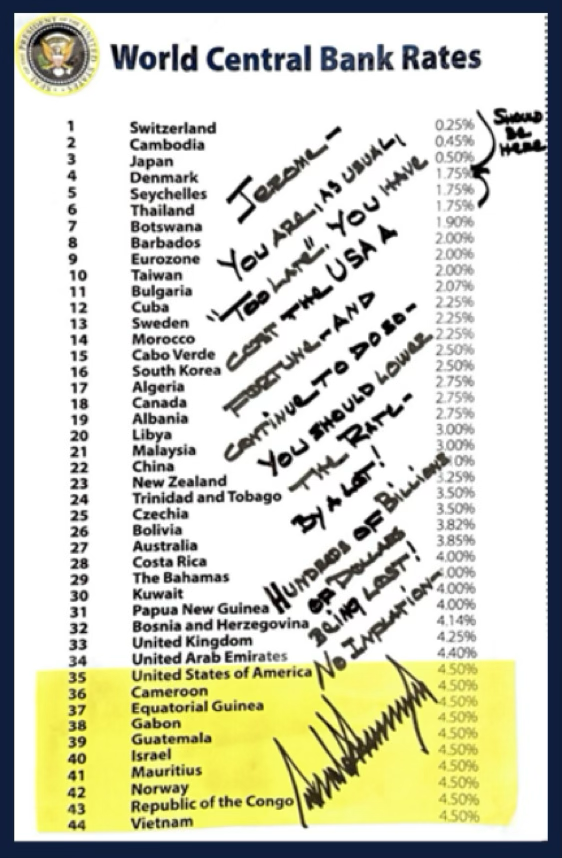

Tensions between President Trump and Federal Reserve Chair Jerome Powell have increased, with Trump calling for Powell’s resignation over persistently high interest rates. Though Powell focuses on inflation risks, the administration is reportedly exploring replacements. Experts note removing Powell before his 2026 term ends would face legal challenges.

The UK manufacturing sector showed early signs of stabilisation in June. The S&P Global/CIPS Manufacturing PMI rose for the third month to 47.7 from 46.4 in May. Though still below 50.0, the upward trend and firms’ ability to raise prices amid rising wages suggest gradual improvement after a prolonged downturn.

China’s economic data was mixed. The official manufacturing PMI edged up to 49.7 in June from 49.5 in May, the first full month post the U.S.–China tariff truce. Despite remaining below expansion territory, the slight gain raises questions about further stimulus from Beijing. The Caixin General Services PMI fell to a nine-month low of 50.6 from 51.1, with slower new business growth and hiring weakness, indicating subdued confidence among service providers.

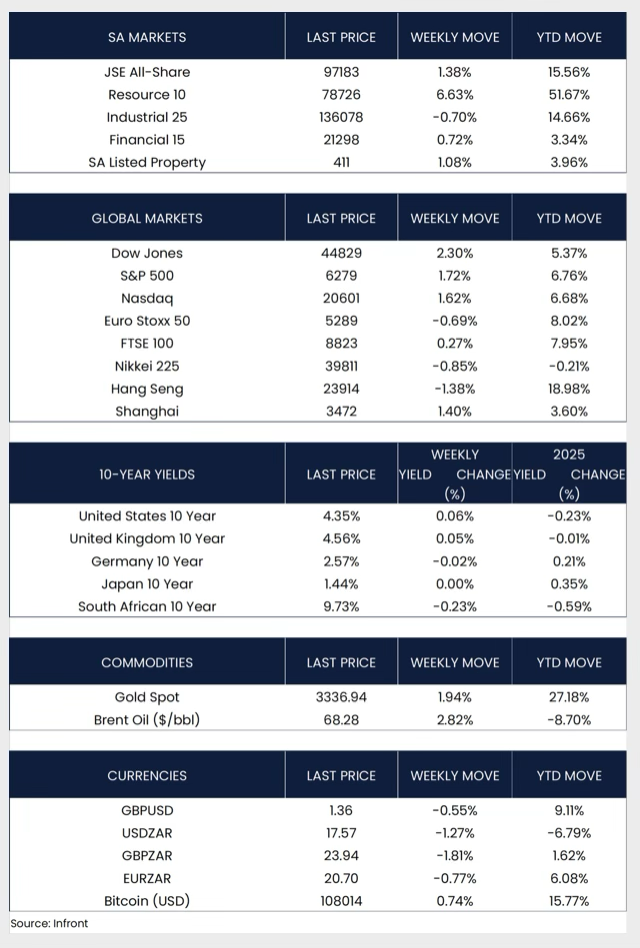

Major U.S. equity indices ended the holiday-shortened week in positive territory. Both the S&P 500 and Nasdaq Composite recorded all-time closing highs for a second consecutive week, gaining 1.72% and 1.62%, respectively. The Dow Jones Industrial Average also advanced, rising 2.30% over the week.

In Europe, performance was mixed. The Euro Stoxx 50 Index declined by 0.69%, while the UK’s FTSE 100 edged slightly higher, ending the week up 0.27%. Asian markets also varied. Japan’s Nikkei 225 Index declined by 0.85%, while mainland Chinese equities posted gains, with the Shanghai Composite Index rising 1.40% in local currency terms. In contrast, Hong Kong’s Hang Seng Index fell 1.38% over the same period.

Market Moves of the Week

South Africa has formally requested an extension to the 9 July deadline for the U.S.'s proposed tariffs on key exports, including steel, aluminium, and automotive products. In an effort to secure a bilateral trade agreement, South Africa has offered to increase imports of U.S. liquefied natural gas (LNG) and proposed capping tariffs at 10% instead of the initially proposed 31%. Discussions between South African trade officials and the U.S. Trade Representative are ongoing as both sides work to align on a new Africa-focused trade framework. The extension aims to provide additional time to finalise terms that protect vital sectors of the South African economy and safeguard approximately 35,000 jobs, particularly in manufacturing and agriculture.

The JSE All-Share Index advanced 1.38% over the week, supported notably by a strong 6.63% gain in the resources sector. Financials and property sectors posted modest gains of 0.72% and 1.08%, respectively, while the industrial sector declined by 0.70%. Meanwhile, the rand strengthened modestly, appreciating 1.27% against the U.S. dollar to close at R17.57 on Friday.

Chart of the Week:

President Trump has called for interest rates to be cut to 1%, criticising the Federal Reserve for keeping policy too tight. The remarks have fuelled renewed scrutiny over Fed independence and raised questions about the future of monetary policy under his administration.

Credits: Strategiq

© 2026 CAPTA Wealth